Sustainability reporting is becoming increasingly prevalent due to the growing consensus that sustainability-related issues can materially affect a company’s performance. This is leading to increased

demand from various stakeholder groups for higher levels of transparency and disclosure about the company’s business activities and performance.

Stakeholders also want information from companies as to how they are responding to issues of sustainable development. This is why companies use sustainability reporting as a tool to disclose their sustainability practices.

Sustainability reporting is not mandatory, but it increases the transparency and accountability of an organization. This in turn helps companies to be better equipped to make profitable decisions which will increase the chances of their long-term success.

Background of BRSR

The BRSR format will enable investors to identify and assess sustainability-related risks and opportunities of the reporting companies, in order to make better investment decisions. It will also act as a medium for companies to demonstrate their sustainability objectives, initiatives, targets and performance

- which will result in long-term value creation.

According to MCA, the objective of BRSR is to serve as a single comprehensive source of non-financial information that includes sustainability data and is relevant to all business stakeholders – shareholders, investors, regulators, and public.

The Structure of BRSR

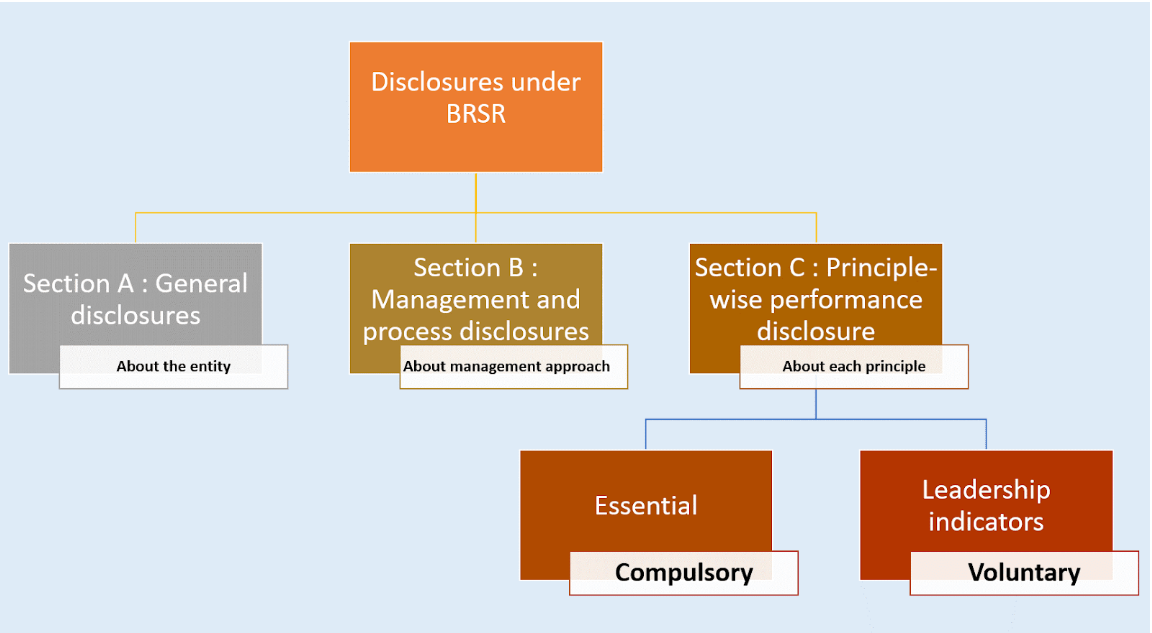

The BRSR format has been divided into three sections. Given below are the purpose and structure of each section:

Section A: General Disclosures

The objective of this section is to obtain basic information about the company – such as size, location, products, number of employees, CSR activities, etc. It also includes additional disclosures on the proximity of a company’s operations to environmentally sensitive sites such as protected areas, water-stressed zones, etc.

Section B: Management and Process

In this section, the company is required to disclose information on policies and processes relating to the NGRBC Principles concerning leadership, governance, and stakeholder engagement. The purpose of this section is to understand whether the business has the right foundation to enable and ensure responsible business conduct. This will help ensure that the policies and processes are imbibed in the core values and functioning of the business.

Section C: Principle-wise performance

This section requires the company to disclose how it is performing with respect to each of the nine principles of NGRBCs. It requires companies to demonstrate their intent and commitment to responsible business conduct, through various actions and outcomes.

The disclosure in this section has been divided into two categories:

1. Essential Indicators are mandatory for all companies

2. Leadership Indicators are voluntary and provide an opportunity for companies to present their impacts and outcomes further

The extent of reporting in BRSR:

The Committee that proposed BRSR found out during its study that only the top 500 listed companies had experience with business responsibility reporting(previous version of BRSR). In order to remove any barrier from reporting, and to nudge more companies to take up sustainability reporting, the committee suggested a two-format approach:

1-Comprehensive BRSR – is a detailed version of BRSR that was developed according to global reporting standards in order to lay emphasis on ESG-related disclosures and contributions toward sustainable development. The format is mandated for the top 1000 listed companies in India, from FY 22-23. Other companies can also opt for this format voluntarily.

2- BRSR Lite – is a pared-down version of which are unlisted companies that are not familiar with sustainability reporting. This version has fewer disclosures in both Essential and Leadership categories, tailored to the extent of information that these companies would be able to provide.

Benefits of reporting via BRSR:

1- Publishing annual BRSR reports is mandatory for top 1000 m-cap companies in India and it's a matter of compliance. Those who voluntarily do it will be seen as leaders in the industry.

2-BRSR is a professional way to disclose sustainability information as it has standardized disclosures on a multitude of ESG parameters, which increases the transparency and accountability of the company.

3-The disclosures in the BRSR format are framed from an ESG perspective and are meant to encourage companies to go beyond merely complying with financial regulations and report on their environmental and social impacts as well.

4-Having a standardized set of disclosures helps a company's stakeholders to assess its business on ESG parameters while understanding the sustainability-related risks and opportunities as well.

Getting started with GRI reporting

To get started with sustainability reporting using standards like BRSR, companies are turning to sustainability management platforms like POSITIIVPLUS. These platforms can help businesses monitor KPIs like energy use, emissions and waste generation, operational costs, and regulatory compliance.Using sustainability management software can help companies gain an understanding of the BRSR format, choose material topics to report on, a report from the variety of available KPIs, aggregate and analyze sustainability performance data, draft a sustainability report, as well as support organizational transparency and communication.